Marcus had built a solid processing book. Twelve years in the payments industry, starting as a W-2 sales rep at a regional ISO, then going independent. By 2023, he had 140 merchants across the Philadelphia suburbs — pizza shops, nail salons, dry cleaners, a handful of sit-down restaurants. His processing residuals cleared $6,200 a month. Not retirement money, but it was recurring, it was predictable, and he had earned every cent of it knocking on doors.

Then he lost Tony's Trattoria. Not because Tony was unhappy with the rates. Not because another agent undercut him. Tony's nephew had shown him Toast at a restaurant trade show. Toast offered a beautiful touchscreen terminal, online ordering, kitchen display, the works — and the processing was baked right in. Tony signed the contract on a Tuesday. By Friday, Marcus's processing relationship with a $65,000-per-month restaurant was gone. Permanently.

Over the next fourteen months, Marcus lost eleven more merchants to Toast, Square, and Clover. Not all of them were restaurants. A boutique switched to Square for its built-in ecommerce. Two salons went to Clover because their landlord's other tenants were on it. Each one followed the same pattern: a bundled POS company showed up, offered a shiny all-in-one system, and the processing went with it.

His monthly residual dropped from $6,200 to $4,100. That is a $25,000 annual pay cut — and the trend was accelerating.

Marcus's story is not unusual. I have heard some version of it from hundreds of agents and ISOs over the past three years. The payments industry is experiencing a structural shift, and agents who do not adapt are watching their income erode merchant by merchant, month by month.

But this article is not a cautionary tale. It is a playbook. Because Marcus figured it out. And by the end of 2025, he was making more than he ever had — processing residuals plus software residuals — with a portfolio that was actually growing instead of shrinking.

Here is what he learned, and how you can do the same thing.

The Structural Problem: Why Processing-Only Agents Are Losing

Let me be blunt about something that many in the payments industry still do not want to hear: if your only value proposition is payment processing, you are in a declining business.

That does not mean processing is declining. Card volume is up. Merchant counts are up. But the number of merchants who will sign with an independent agent for processing alone is shrinking every quarter. Here is why.

Bundled POS Companies Have Changed the Game

Toast, Square, and Clover are not really POS companies. They are payment processing companies that built software around the processing. Their business model is simple: give the merchant a compelling software experience, and capture the processing revenue for themselves.

When Toast walks into a restaurant, they are not selling a credit card terminal. They are selling a kitchen display system, online ordering, payroll, team management, and a beautiful front-of-house interface. Oh, and by the way, the processing is included. The merchant never even thinks about who their processor is.

This is the fundamental problem. The agent who only sells processing has no defense against a competitor who bundles processing with software. You are bringing a knife to a gunfight.

The Numbers Tell the Story

Consider what has happened in the restaurant vertical alone:

- Toast now processes for over 120,000 restaurants — every one of those merchants was taken from an existing processor or agent

- Square has expanded from micro-merchants to full-service restaurants and retail, pulling processing in-house for each one

- Clover is Fiserv's trojan horse — agents who sold Clover thinking they were protecting their processing book later discovered Fiserv controls the relationship, not them

If you are an ISO or independent agent reading this, ask yourself: how many merchants have you lost to bundled POS companies in the last two years? And how many are you likely to lose in the next two?

The Solution: Control the POS Relationship to Protect the Processing

Here is the insight that changed Marcus's business, and it is changing the business of smart agents across the country: if the POS is how merchants get captured, then you need to be the one selling the POS.

But not just any POS. The wrong POS partnership will make the problem worse, not better. You need a POS platform that does three critical things:

- Processor-agnostic — It must work with YOUR processing. If the POS company controls the processing, you are just handing your merchants to a different captor.

- Genuinely competitive — It must go toe-to-toe with Toast, Square, and Clover on features. Merchants will not accept a second-rate system just because you are their agent.

- Multi-vertical — It should work for restaurants, retail, beauty/spa, and more. You call on all kinds of merchants. Your POS should serve all of them.

This is where KwickOS comes in, and why it has become the platform of choice for a growing number of ISOs and payment agents who are serious about building long-term residual income.

Why KwickOS Is Built for Payment Agents

I want to be specific about what makes KwickOS different, because there are other processor-agnostic POS systems out there. The difference is that KwickOS was designed from the ground up to work with payment agents, not around them.

Processor-Agnostic by Design

KwickOS integrates with any payment processor — Fiserv, TSYS, Worldpay, Global Payments, Elavon, or any ISO's proprietary gateway. When you sell KwickOS to a merchant, you place them on YOUR processing. The merchant runs KwickOS for the software. They run your processing for the payments. Two separate relationships, both generating revenue for you.

KwickOS will never compete with you on processing. That is not a marketing promise — it is a structural feature of the platform. The company makes money on software subscriptions, not interchange. Your processing residual is yours, period.

A Platform That Wins Against Toast and Square

Your merchants are being pitched by Toast reps on a weekly basis. If you hand them a POS system that feels outdated or limited, they will switch anyway. KwickOS is not a lightweight alternative — it is a full operating system for running a business:

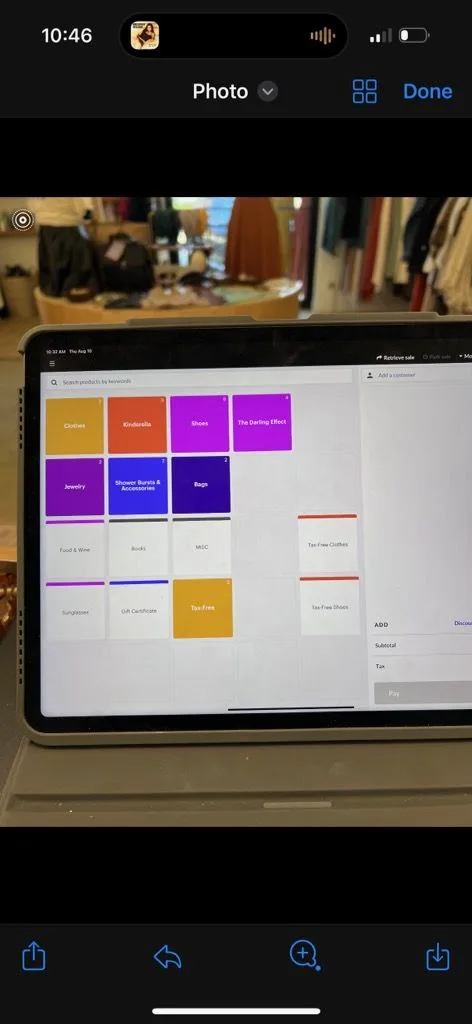

- KwickPOS — Point-of-sale and checkout with full restaurant and retail configurations

- KwickMenu — Digital menu boards and QR code ordering

- KwickSign — Digital signage across the business

- KwickPhone — AI-powered phone ordering system

- KwickPay — Payment integration (with YOUR processor)

- KwickPhoto — Professional food photography for menus and marketing

- KwickTracker — Delivery and order tracking

- Online ordering, kitchen display, CRM, loyalty, staff scheduling, inventory — all built in

When a Toast rep walks into your merchant's restaurant, the merchant can honestly say: "I already have all of that. And my system works with my existing processor." That is the conversation you want your merchants having.

One Platform, Every Industry

Most agents call on merchants across multiple verticals. You might board a restaurant this week and a hair salon next week. With a single-vertical POS like Toast (restaurants only) or Lightspeed (retail-focused), you need different solutions for different merchants. That means multiple vendor relationships, multiple training programs, multiple support channels.

KwickOS runs restaurants, retail stores, beauty and spa businesses, grocery, butcher shops, and more — all from the same platform. One partnership, one set of training, one support team. Your addressable market just expanded to every SMB merchant you encounter.

The Revenue Math: How Agents Hit $10K/Month

Let me walk through the actual numbers, because this is where the model gets exciting. When you sell KwickOS alongside your processing, you are stacking two independent residual streams on every merchant.

Stream 1: Processing Residuals (What You Already Know)

| Merchant Type | Monthly Card Volume | Agent Residual at 0.15% |

|---|---|---|

| Small restaurant / cafe | $20,000 - $30,000 | $30 - $45/month |

| Mid-size restaurant | $40,000 - $60,000 | $60 - $90/month |

| Busy full-service restaurant | $80,000 - $120,000 | $120 - $180/month |

| Retail store | $30,000 - $50,000 | $45 - $75/month |

| Beauty / spa | $15,000 - $30,000 | $22 - $45/month |

A typical agent with 50 merchants averaging $40,000/month in card volume at a 0.15% residual earns roughly $3,000/month in processing residuals. That is the baseline most experienced agents are already familiar with.

Stream 2: KwickOS Software Residuals (The New Revenue)

When you sell KwickOS, you earn a recurring monthly software residual on each merchant account. This is revenue that did not exist before in a processing-only model. The software residual is paid for the life of the account, just like your processing residual.

The Compounding Effect

Unlike one-time bonuses or hardware markups, both streams are recurring. Every new merchant you board increases your monthly income permanently. You are not starting from zero each month — you are building on top of last month's base. This is the same compounding dynamic that makes processing residuals so powerful, but now you have two engines instead of one.

Putting It Together: The Path to $10K/Month

| Portfolio Size | Processing Residuals | Software Residuals | Combined Monthly |

|---|---|---|---|

| 25 merchants | $1,125 - $1,875 | Additional recurring | Growing base |

| 50 merchants | $2,250 - $3,750 | Additional recurring | Significant income |

| 75 merchants | $3,375 - $5,625 | Additional recurring | Strong income |

| 100+ merchants | $4,500 - $7,500 | Additional recurring | $10,000+/month |

Agents who build a portfolio of 100 or more merchants on KwickOS with their own processing are consistently clearing $10,000 per month or more in combined residuals. And unlike a W-2 sales job, this income does not disappear when you take a vacation. It is yours as long as the merchants are active.

(100 merchants at 0.15%)

(additional per merchant)

(100+ merchant portfolio)

(growing as you add merchants)

But Here Is What Really Matters: Retention

The revenue math only works if your merchants stay. And this is where the KwickOS model has a structural advantage over processing-only relationships.

When you only sell processing, the merchant has no reason to stay loyal. Processing is a commodity. The next agent who walks in with a rate that is two basis points cheaper can flip them. Your average merchant lifespan might be 2-3 years.

When you sell KwickOS plus processing, the merchant is running their entire business on your platform. Their menu is in KwickOS. Their staff schedules are in KwickOS. Their online ordering runs through KwickOS. Their customer loyalty data lives in KwickOS. Switching costs are real and significant. Merchant lifespan extends to 5-7 years or more.

The deepest moat in the payments business is not price — it is dependency. When a merchant's daily operations depend on your platform, they do not switch over a few basis points. This is exactly why Toast keeps winning merchants from processing-only agents. Now you can use the same strategy, but with you controlling both sides of the relationship.

The KwickOS Partner Advantage: What You Get

I have evaluated dozens of POS partner programs for ISOs and agents. Here is what makes the KwickOS program stand out for payment professionals specifically.

Free Demo Hardware Kit

Qualified partners receive a demo hardware kit at no cost. If you have ever tried to sell POS systems using a slideshow presentation, you know the close rate is abysmal. Merchants need to touch the screen, see the interface, watch how fast a ticket prints. The demo kit lets you walk into any merchant and give them a live, hands-on experience. This alone can double or triple your close rate.

Dedicated Partner Success Manager

You are not calling a general support line. You have a named partner success manager who knows your portfolio, helps you with technical questions during the sales process, and supports you through installation and onboarding. When you are sitting across from a merchant and they ask a question you cannot answer, you have someone to call who picks up the phone.

30 Years of IT Expertise, 20 Years in Restaurants

The team behind KwickOS is not a Silicon Valley startup that discovered restaurants last year. This is a company with three decades of IT infrastructure experience and two decades working specifically with restaurant and retail operators. That experience shows up in the product — in the kitchen display workflows, the Chinese restaurant configurations, the multi-location management tools. When your merchant has a problem at 8 PM on a Saturday night, this team has seen it before and knows how to fix it.

5,000+ Active Merchants

This is not a beta product. Over 5,000 businesses run on KwickOS today. That install base means the software has been battle-tested in real-world conditions across every type of merchant you will encounter. When a prospect asks "who else uses this?" you have thousands of references.

The Competitive Comparison: KwickOS vs. Selling for Toast, Square, or Clover

| Factor | Selling Toast / Square / Clover | Selling KwickOS + Your Processing |

|---|---|---|

| Processing relationship | POS company controls it | You control it |

| Processing revenue | Reduced or zero residual | Full residual is yours |

| Revenue streams | Referral fee or small residual | Processing + software residuals |

| Merchant loyalty | Merchant is loyal to the POS brand | Merchant is loyal to you |

| Portfolio ownership | POS company owns the relationship | You own the relationship |

| Industry coverage | Usually single-vertical | Restaurant, retail, beauty, grocery, more |

| If you leave the program | Merchants stay with the POS company | Processing relationship stays with you |

Look at that last row carefully. If you build a portfolio on Toast and decide to leave or if Toast changes your terms, your merchants are gone. They are running Toast software and Toast processing. You have no leverage and no recourse.

With KwickOS, the processing relationship is always yours. If you ever need to make a change on the software side, your processing book remains intact. You have built equity in something you actually own.

What Happened to Marcus

Remember Marcus from the beginning of this article? After losing eleven merchants to bundled POS companies, he realized his processing-only model was a dead end. He started researching processor-agnostic POS platforms and found KwickOS.

Here is what his first twelve months looked like:

- Months 1-2: Got the demo hardware kit, completed partner training, and identified 15 merchants in his existing book who were at risk of leaving for Toast or Square. He proactively re-approached them with KwickOS as a technology upgrade — no processing change needed.

- Months 3-4: Converted 8 of those 15 at-risk merchants to KwickOS. Processing stayed the same, but now they had modern POS software and no reason to look at Toast. He stopped the bleeding.

- Months 5-8: Started prospecting new merchants with a combined KwickOS + processing pitch. His close rate went up because he was no longer selling just processing — he was selling a complete business platform. He boarded 20 new merchants.

- Months 9-12: Hit a rhythm. By month twelve, he had 65 merchants on KwickOS with his processing. His monthly income was higher than it had ever been — and more importantly, his merchant retention rate was higher than at any point in his career.

Marcus did not become a technology expert overnight. He did not learn to code or become a POS installer. He leveraged his existing skills — merchant relationships, consultative selling, knowledge of payment processing — and added a platform that made those skills more valuable.

Marcus puts it simply: "I used to sell processing and hope the merchant did not get poached by a POS company. Now I sell the processing AND the POS. There is nothing left for Toast to pitch them on."

How to Get Started

If you are an ISO, independent agent, or payment professional reading this, here is the honest assessment: the window to make this transition is open, but it will not stay open forever. Every month that goes by, more of your merchants get pitched by bundled POS companies. The agents who move now are the ones who will build the largest portfolios.

Here is the practical path forward:

- Audit your current book. Identify which merchants are running legacy POS systems or no POS at all. These are your highest-risk accounts — and your easiest KwickOS conversions.

- Apply for the KwickOS partner program. The qualification process is straightforward. If you have an active processing book and a track record of merchant sales, you are likely a fit.

- Get your demo kit and complete training. KwickOS provides hands-on training so you can confidently demonstrate the platform. You do not need to be a POS technician — KwickOS handles installation and support.

- Start with your existing merchants. The easiest first sales are merchants who already trust you. Offer them a technology upgrade that works with their existing processing (which is already with you). No disruption, just a better system.

- Expand to new prospects. Now you are walking into cold prospects with a complete solution: modern POS + competitive processing. That is a fundamentally stronger pitch than processing alone.

Ready to Double Your Residual Income?

Join the KwickOS partner program. Keep 100% of your processing revenue. Sell one platform for restaurants, retail, beauty, and more. Free demo hardware kit for qualified partners.

Apply for the Partner ProgramThe Bottom Line

The payments industry is not dying. But the processing-only agent model is under serious pressure, and pretending otherwise is not a strategy. The agents who are thriving in 2026 are the ones who recognized this shift early and positioned themselves as platform providers, not just processing providers.

KwickOS gives you the tool to make that shift without sacrificing the processing relationships you have spent years building. You are not replacing your processing business — you are fortifying it with a software layer that makes it stickier, more valuable, and harder for competitors to displace.

Processing residual plus software residual. Two income streams from every merchant. A portfolio that grows instead of shrinking. That is how agents are building $10K/month residual income — and that is the model that will define the next decade of the payments industry.

The question is not whether you should make this move. The question is whether you will make it before your competitors do.